Important: Patient Advocate Foundation’s TotalAssist program launches on July 1. Whether you’re a new patient, or you’re currently receiving assistance from Patient Advocate Foundation or PAN Foundation, visit our TotalAssist.org website to learn more about next steps, get helpful information, and access your portal account. Starting July 1, the call center can be reached by calling toll free, 866-512-3861 from 8:30am to 5:30pm ET.

Information about this website: Following the March 2026 merger of Patient Advocate Foundation and the PAN Foundation, this website is now a part of Patient Advocate Foundation and remains active during our website transition.

Where to find information during our transition:

- About the merged organization: uniting.patientadvocate.org

- Financial assistance: totalassist.org

- Additional direct patient services and resources: patientadvocate.org

- Education: panfoundation.org and education.patientadvocate.org

- Clinical trials education: clinicaltrials.panfoundation.org

- Advocacy: npaf.org

- Research: patientinsightinstitute.org

Learn about and advocate against these harmful programs for people with commercial insurance.

In recent years, commercial health insurers have adopted programs and policies that are hurting patients. These programs limit access to medications, increasing the amount patients have to pay out-of-pocket for their care.

Unfortunately, patients often don’t know that these programs are part of their health plans. They often learn about the programs when their insurance company denies medications. Or they are at the pharmacy counter and are surprised by their out-of-pocket cost.

We invite you to learn about three of these harmful programs below, including copay accumulators, copay maximizers, and alternative funding programs. These programs may prevent patients from adhering to treatment. So, it is important that patients and healthcare professionals understand how they work. In addition, learning how they can advocate against these harmful programs.

Copay accumulators

What is a copay accumulator?

Copay accumulators are programs used by insurance plans that affect how copay assistance is applied to deductibles and out-of-pocket costs.

People living with serious illnesses are often prescribed medications with high out-of-pocket costs. Many patients find it challenging to afford these costs. This is why they often turn to financial assistance provided by pharmaceutical manufacturer programs, charitable foundations, friends and family, and faith-based communities. This financial help usually counts toward the patient’s annual deductible or out-of-pocket maximum, based on their health plan.

But that isn’t the case for patients whose health plans have a copay accumulator program in place.

How copay accumulators work

Copay accumulator programs are typically offered by plan pharmacy benefit managers (PBMs). They permit patients to use third-party copay assistance for covered drugs without counting that assistance towards a patient’s deductible or out-of-pocket cost sharing requirements.

Once a patient has exhausted the available third-party copay assistance, the patient remains responsible to pay their entire deductible and all other out-of-pocket cost-sharing requirements as if no third-party copay assistance has been collected by the plan/PBM.

These programs are complex, so we’ve shared two scenarios below to help explain how they work.

For example, let’s consider a patient named Arthur, who is living with a chronic illness. Arthur has an annual deductible of $2,500 and a $500 manufacturer copay coupon for his medication.

- If Arthur’s plan does not have a copay accumulator program, the $500 coupon will count toward his annual deductible: $2,500 – $500 = $2,000. Arthur will be responsible for the remaining $2,000 before reaching his annual limit.

- If Arthur’s plan has a copay accumulator program, the $500 coupon will not count toward his annual deductible: $2,500 – 0 = $2,500. Arthur must pay the full $2,500 before satisfying his annual deductible.

When health plans include copay accumulator programs, patients pay more out of pocket for their treatment. It also takes them longer to reach their annual deductible and out-of-pocket limits.

The Crohn’s & Colitis Foundation shared a similar example of how copay accumulators work in the illustration below:

The impact of copay accumulators on patients

Unfortunately, copay accumulator programs are often put in place with little or no notice or education for patients. Accumulator programs negatively impact patients in several ways:

- They can lead to poorer health outcomes and may add costs to the entire health system. This happens when patients choose to not start taking a medication at all, or to skip doses and not follow the treatment as prescribed by their healthcare provider.

- They result in increased costs for the patient. This can be particularly challenging for people with high-deductible health plans.

Copay Maximizers

What are copay maximizer programs?

Copay maximizer programs are used by health plans/PBMs to “maximize” the value of third-party copay assistance (typically manufacturer copay assistance) available for a particular covered drug in a plan year. Copay maximizer programs work by the plan/PBM designating a drug as a covered non-essential health benefit (covered non-EHB) and then setting the patient’s required annual copayment for that drug equal to the maximum amount of available manufacturer financial assistance in that plan year, an amount that may exceed permissible patient cost-sharing protections under the Patient Protection and Affordable Care Act (ACA).

With a maximizer, a patient must enroll in the program through a third-party administrator before they are permitted to fill that prescription under the terms of the plan. If the patient does not enroll in the copay maximizer program, they will be responsible for 100% of the cost of their drug.

Once the third-party copay assistance has been exhausted, the patient typically has no remaining financial liability for the drug; however, due to its designation as a “covered non-EHB,” nothing paid for the drug counts towards their deductible or maximum out-of-pocket for the patients other covered services.

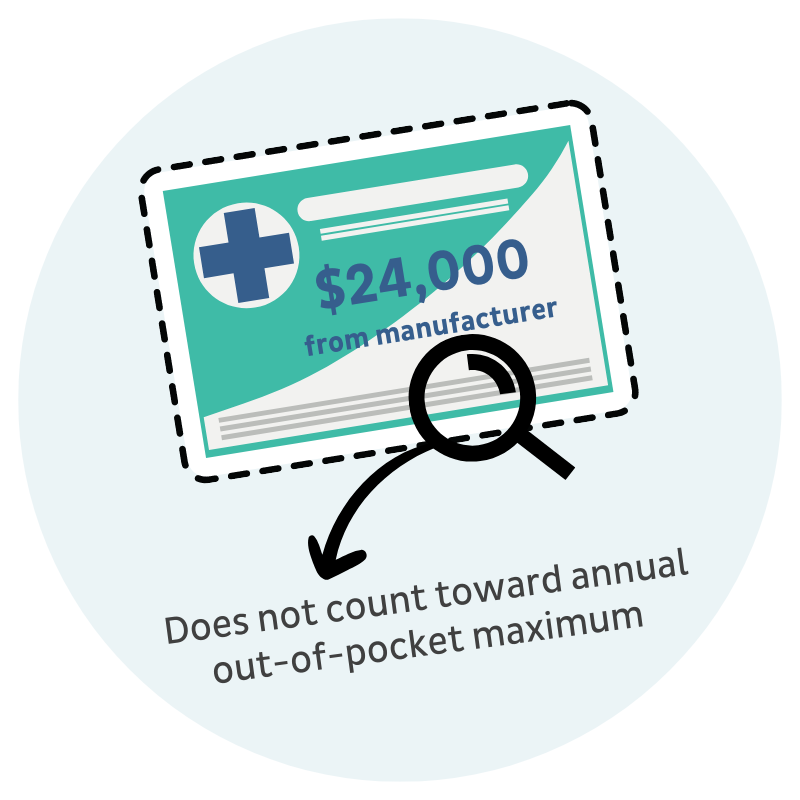

For example, let’s say that Ariel needs a specialty medication for her rare disease. There is $24,000 in manufacturer copay assistance available per year for her medication. Ariel’s health plan determines that her copay is at least $2,000 per month—$24,000 in available copay assistance divided by 12 months in the plan year.

In Ariel’s example from above, she has two choices:

- She can join the copay maximizer program and use a manufacturer’s coupon to cover the $2,000+ monthly copay. She will have little or no upfront cost for her medication, but these payments will not apply to her annual out-of-pocket maximum.

- Or she can choose not to join the copay maximizer program and face the $2,000+ copay each month on her own. Her payments will not apply to her annual out-of-pocket maximum in this scenario either.

The impact of copay maximizers on patients

Maximizer programs negatively impact patients in several ways:

- They disproportionately impact individuals who are seriously or chronically ill. Faced with increased out-of-pocket costs, patients may choose not to start taking a medication at all, or to skip doses and not follow the treatment as prescribed by their doctor. This may lead to poorer health outcomes.

- They may cause patients to face significant out-of-pocket costs if they don’t sign up for a maximizer program. These costs may exceed their plan’s out of pocket maximums. Their costs may also exceed the out-of-pocket maximums established by the Affordable Care Act.

- They hurt patients in the long run. This is due to payments coming from the manufacturer copay assistance program not applying to a patient’s annual deductible.

- They are also why some health plans are restricting access to essential health benefits. Plans are claiming that more and more specialty medications are non-essential and therefore do not have coverage. Non-essential health benefit schemes like copay maximizers violate the Affordable Care Act (ACA). Under the ACA, patient contributions for essential health benefits, like prescription drugs, must count towards their annual out-of-pocket limits. (Read more about essential health benefits below)

What are essential health benefits under the ACA?

Prescription drugs are one of the ten essential health benefit (EHB) categories listed in the Affordable Care Act (ACA). The ACA does not specifically define “prescription drugs.” However, it refers to them broadly as FDA-approved drugs. Specialty medications are FDA-approved drugs, often prescribed to treat life-threatening, chronic, and rare diseases.

Health plans can adopt their own definition of EHBs. But their definition must be consistent with guidelines from the U.S. Department of Health and Human Services (HHS). To date, HHS has stated that plans can only exclude a name-brand prescription drug from coverage when the plan offers a generic alternative.

So that means when a health plan broadly categorizes specialty medications as non-essential health benefits without a generic alternative available, they are using an unauthorized definition of prescription drugs.

Violation of ACA’s cost-sharing requirements

Under the Affordable Care Act (ACA), all essential health benefits, including prescription drugs, have annual limits on cost-sharing, unless an exception exists. Cost-sharing includes deductibles, coinsurance, copayments, and similar charges.

The HHS has also stated that if a patient pays for and receives a prescription medication that isn’t covered under the general health plan, the plan must consider this medication an essential health benefit and count the patient’s out-of-pocket payments toward the plan’s annual limit on cost-sharing. So, programs that prevent payments for specialty medications from counting towards a patient’s annual limits are not in compliance with the ACA’s cost-sharing requirements.

What’s being done to protect people from copay accumulators and copay maximizer programs?

State legislation

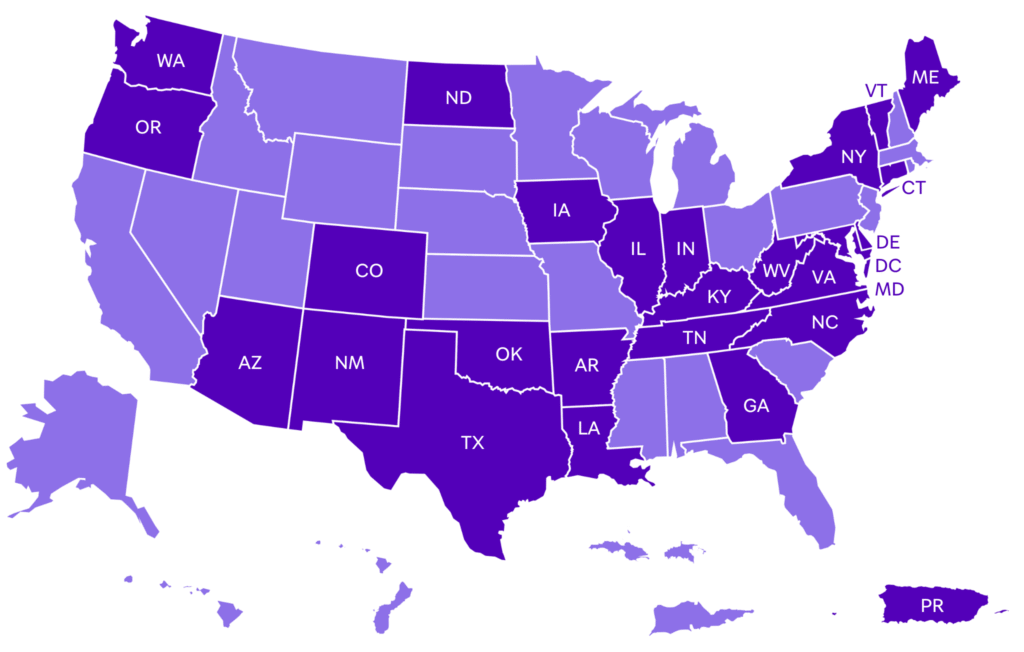

To date, many states, the District of Columbia, and Puerto Rico have passed legislation to ban these programs.

In each of these states and territories, legislation requires insurers to count copay assistance paid by or on behalf of a patient towards their annual deductible and out-of-pocket maximum. The laws primarily target copay accumulators but some also ban copay maximizers.

State legislation applies to state-regulated individual and family plans and fully funded small group health plans. It does not apply to self-funded employer plans or large group plans. Unfortunately, state legislation does not stop plans from determining that specialty medications are non-essential health benefits.

Federal legislation can ban copay accumulator programs

While state legislation applies to state-regulated individual and family plans and fully funded small group health plans, it does not apply to self-funded employer plans or large group plans. Unfortunately, state legislation does not stop plans from determining that items and services, like specialty medications, are non-essential health benefits.

At the federal level, the Help Ensure Lower Patient (HELP) Copays Act will be most impactful.

The HELP Copays Act requires health plans to count the value of copay assistance toward a patient’s cost-sharing requirements. The bill clarifies the Affordable Care Act definition of cost-sharing to ensure payments made “by or on behalf of” patients count towards their annual deductible and/or out-of-pocket maximum.

The legislation also states that any item or service covered under a plan is an essential health benefit and that cost-sharing for these items must count towards a patient’s out-of-pocket maximum.

The HELP Copays Act was re-introduced (S.864) by Senators Tim Kaine (D-VA) and Roger Marshall (R-KS) in March 2025.

Three things you can do about copay accumulator and maximizer programs

#1 – Understand your policy

You should become familiar with your insurance policy documents and know if your plan includes a copay accumulator or maximizer program. People with employer-sponsored insurance plans, particularly people enrolled in high-deductible health plans (HDHPs), are most likely to have a copay accumulator or maximizer plan in their policy. HDHPs have become popular as employers and insurers try to lower their costs. When selecting insurance plans, it is important to understand your health plan’s deductible and your cost-sharing requirements.

Unfortunately, it can be quite difficult for patients to know if their plan has a copay accumulator or maximizer program in place—language differs from plan to plan.

These terms can all mean a plan includes a copay accumulator or maximizer policy:

- Copay accumulator (adjustment) program

- Copay maximizer program

- Benefit plan protection program

- Out-of-pocket protection program

- True accumulation

- Variable copayment

- Out-of-pocket maximum calculation

- Primary coupon adjustment

#2 – Become an advocate

Ask your elected officials to support The HELP Copays Act and ban copay accumulator programs.

If you live in a state that has not banned copay accumulators:

- Contact your House representative

- Contact your state’s insurance department

- Tell your employer! It is possible that your employer may not be aware that they signed up for this program and may not realize the potential negative impact of the program has on their employees.

#3 – Share your story with PAN

If you have experienced the impact of a copay accumulator or maximizer program, we would love to hear from you. Your story helps others understand the impact of these programs.

Alternative funding programs

Understanding alternative funding and specialty drug carve out programs

Health plan sponsors, like employers that fund their own health coverage, may use alternative funding programs to save money by excluding some or all specialty medications from coverage, labeling them as non-essential health benefits. Since the health plan does not cover these specialty medications, a patient’s out-of-pocket spending will not count toward their annual deductible. Patients are then directed to alternative funding programs—also known as specialty drug carve out programs— operated by vendors that are separate from their health plan and are not health insurance.

These vendors work to connect patients with financial assistance through a drug manufacturer or charitable assistance program, disguising patients as uninsured, if necessary. Technically, these patients have no coverage for these medications. Vendors may even direct patients to illegally import medications internationally. But help paying for these medications is not guaranteed from any of these sources.

How these programs work:

- The patient is told that they must enroll in an alternative funding program and is referred to a private company, often called an alternative funding vendor. Vendors operate separately from the patient’s health plan.

- The vendor contacts the patient and offers to help find an assistance program to access their specialty medications.

- If the patient agrees to work with the vendor, the patient may be able to get their medication for little or no out-of-pocket costs if a patient assistance program is available and if the patient qualifies.

- The vendor collects the patient’s personal information, such as household size and annual income, to determine the type of third-party financial assistance the patient is eligible for.

- Vendors then determine whether patients are eligible for manufacturer copay assistance programs, charitable assistance programs, or international importation programs.

- The vendor helps patients disguise themselves as uninsured so they can apply for patient assistance programs to cover the cost of the prescriptions. (Keep in mind that while these patients have health coverage, their plan states that they are not covered for the specialty medications they need.)

- If no patient assistance program is available or if the patient fails to qualify, then the patient can be denied access to the medication or forced to pay out of pocket on their own. If assistance can’t be found or a patient can’t qualify, their health plan also has the option to override the original designation as a non-essential benefit, which allows the patient to resubmit a request for prior authorization for their specialty medications.

- If the patient refuses to work with the alternative funding vendor, then the patient will be denied access to the medication unless they self-pay.

- If the patient does not enroll, they will be responsible for 100 percent of the cost of the medication that is deemed non-essential. As a non-essential medication, any cost paid for the medication by or on behalf of the patient will not count towards their deductible or annual limit on cost-sharing.

- If the patient is eligible for a different program, like one that imports internationally, then the patient will receive their medication through that source. Some vendors will try to get products from pharmacies located outside the United States, but this is not permitted based on guidance from the Food and Drug Administration (FDA).

Access to specialty medications prescribed by health care professionals should be deemed an essential health benefit, and their costs should be covered by health plans. Patient assistance programs should be reserved for those who meet their specific eligibility criteria, based on need.

Federal legislation can ban alternative funding programs

Currently, there is no legislation pending that would prohibit the use of alternative funding programs. It is possible that there will be growing interest from Congress and the patient advocacy community stands ready to advocate to ban these harmful programs.

Three things you can do about alternative funding programs:

#1 – Understand your policy

If your plan has told you that your specialty medication is not essential, or that specialty drugs are excluded from the plan’s formulary and that another company can help you find financial assistance, then you may be involved in an alternative funding program scheme. When selecting insurance plans, it is important that you understand the health plan’s policy on including/excluding specialty medications on formulary.

#2 – Become an advocate

Let your elected officials know that alternative funding programs harm patients and should be abolished. Reach out to your members of Congress to share your story.

#3 – Share your story with PAN

As alternative funding programs become more common, one of the most important things we can do is track and share stories about how these programs are negatively impacting patient care. With alternative funding programs, patients face delays in their care and have the additional burden of sharing personal, financial, and medical information with external private companies just so that they try to find funding. If funding sources are not found, patients may have to delay starting their treatment, which could impact their health outcomes. If you have experienced an alternative funding program, we invite you to share your story.

A guide for healthcare professionals

PAN has created an educational guide to help healthcare professionals and providers understand alternative funding programs, copay accumulators, and copay maximizers.

-

Subscribe to news

Sign up to receive PAF news, from helpful articles to action alerts.

Subscribe today -